Max short? Or a long term bottom?

AEO stock pitch, data centers, and CTAs!

Here’s a weird historic- not really adage, but more factoid. Years that end in ‘5 tend to be some of the best investment years of the decade and rarely go down. I think there’s only one negative ‘5 years since 1900. Forget seasonality, this year has been the worst ‘5 year since ever in Q1. Normally ‘4 years aren’t great, at least until after the elections, which causes the damage that the ‘5 years heal, but with how good last year was it has flipped.

This could be from recessionary risks. It could be because of Tariffs it could be for many reasons we don’t know. What I do think is that the first act of 2025 has been complete. We’ve priced in recession risks up almost to 50/50 (more on this below), the EU and China have run on valuations and finally stimulating, and it turns out Trump’s first 6 months might be deflationary…..At least no one saw that last one coming.

So now we’re onto act two of the year. Who knows how long this one lasts, or what it looks like specifically. I do imagine it leads with a bounce. To 5800? 5900? New ATHs? That’s unknown. Also unknown is if it will lead to us heading lower before the end of the year. But I will say that easy money on the short side has likely been made. At least for a few weeks. More on this below. Let’s talk about Friday.

There is an old trading adage. ‘The market doesn’t bottom on a Friday’. Historically, when the market is weak, like it has been this week, even with a rally on Friday the weekend gives traders and investors times to digest the market movement and create a plan of action. Aka sell. Even if Friday is green this usually leads to a weaker Monday, and then Turnaround Tuesday! Where the market often finds support after the Monday morning sell, or at close, then launches on Tuesday. Leading all those late sellers off sides and now suddenly chasing the prices higher and higher.

Its for this reason when I started to outline this weekend recap near close and the S&P 500 still unable to break 5630 that I was going to lead with ‘be cautious but optimistic for the next week, as until we’re able to push through the 5630 seller we haven’t done much’. I was going to point to the fact that CTAs take on a more influential role when there’s less liquidity in the system, and that they’re close to max short. I was going to mention how its clear some stocks have started to find some support so we can start to put some risk on, but not aggressively (more on these names below). But broadly I was going to say the opening part of the week is time to be cautious, at least until we see real buyers step in, not just short covering blowing out last shorts in.

That outline has somewhat changed with the close. There is still a lot of reasons to be cautiously optimistic next week, with some weakness expected on Monday into a powerful back half of the week, but with us firmly above the JPM collar again, and possibly having broken the 5630 seller, the indexes are looking half way decent.

Friday was a 91% up day, which is very strong. Means unlike on Wednesday which was sloppy and only had a few advancers, the broad market was participating in the rally. This is good. This is the kind of price action you want to see to say we’ve bottomed. At least near term. It was also a nice reprise from the insanity of the first few days of the week.

If we can open and hold 5630 on the index we’re likely to see solid to explosive upside near term. Even if we have some small amount of sell left on Monday or any day next week. I think this open would point to the worst of this part of this pullback being behind us. To continue lower the macro data needs to start printing recessionary data. Which is yet to be determined. Something we need to watch, but nothing we’ll know in either direction in the next 10 sessions.

We did get some solidly bullish data on DC this week. A ‘clean’ CR was passed through the Senate. This likely means Fiscal flows will turn back on next month. I mentioned these back in January as why I thought it was difficult to be bullish after Trump was in office through tax season. There was a lack of these flows because Yellen emptied her accounts on the way out the door. Did I think it was going to be this bad…..sort of as I had recommended buying QQQ 480 puts out to April. But not nearly this quickly as I closed my personal puts three trading days in March, losing that protection as the market fell into hades.

The other bullish note is that some names are at least starting to get so cheap that even in a recession they’re a solid buy at these levels. This is important because when things get to these levels fundamental buyers’ step in, ones who have longer time lines and don’t trade like insane pod shops.

The nice part of when the market is puking is that they often throw the baby out with the bathwater. There’s a handful of stocks that I think have 2x upside over the next 18 - 24 months, many of which I’ve talked about before. But today I wanted to introduce a new name to some. American Eagle Outfitters Inc (AEO).

They had earnings on Wednesday and while they crushed their numbers, much like every other retailer that’s reported in the last two weeks they were hesitant in their guidance. This caused the stock to drop as low at 10.45 per market on Thursday morning, which was down 10% from the close. The stock finished the week down 2.5% from prior to its earnings print at $11.14. Here’s what makes AEO interesting. Going into the print the street had them doing 1.75 - 1.85 in EPS before management talked down their 25 numbers. Some analysts even had them within spitting distance to $2 a share. $1.75 a share would’ve put them flat in EPS yoy, but prior to this call management had talked about trying to get to 6b in revenue by Jan 2027. Which would’ve been 6% annual growth in top line. Management had also talked about they had plans to expand margins, which had been working out, again until they talked down the next twelve months.

Now the street is expecting $1.5 in earnings at the mid point. That puts them at 7.5x NTM earnings. This is with some recession risks built in now. If we assume that management was sandbagging, or that a consumer spending pullback isn’t going to be a long term trend because the economy is fine, then its more likely that their 2025 EPS comes in close to $2 a share. North of where the street was prior. Even at $1.9 a share its at less than 6x NTM EPS. Add in a .5 a share dividend a yield of 4.4% can help you weather some weakness in the share price near term. Its cheap and it pays you to own it, win win!

Now you’re likely saying, so what if its cheap, there are a 5,000 stocks that are cheap and/or cheaper than they were a few months ago. You’re right. What makes American Eagle interesting is its growth.

AEO is really two businesses, with a few other smaller fast growing brands that don’t move the needle yet, but might soon. The two big brands the namesake, American Eagle, which is as a now historic Americana brand, its well known not just domestically but around the world. The downside to being older, is unless it manages to convince girls that they look better in unflattering baggy jeans like Abercrombie and Fitch was able to do, it basically grows at inflation rate plus a little bit. The real value add for management is in margins and inventory. Two things they were doing well at coming into this print.

The real growth story is the AERIE. A clothing brand focused on the TikTok generation. One that is doing so quite successfully I might add. They’re growing same store sales at 6%+ in a non recessionary environment and have (had) a pretty clear path to 8% SSS growth. Aerie currently accounts for just over 33% of AEOs sales, but with their growth and separate(ish) branding, its possible that number could be north of 40% by 2027, still growing at 6 - 8%. If Aerie was a stand alone company it would be trading at 12x (with recession risk priced in) and 15 - 16x without it. If you wanted to assume the legacy brand is a zero, then Aerie already trades at about 14 - 16x NTM EPS via AEO.

AEO is the kind of company you want to buy when there’s a massive pullback. Even if we hit a recession soon its very cheap. So the downside case is limited unless you think we’re going into another GFC spending collapse. If that is your base case you probably want to pass on AEO. With recession risks pointing to a downside of the mid to high 9s at the lowest, with a 4.5% dividend covering half of that pullback, your potential net loss is somewhere between 5 - 7% over the next year (including the dividend). If we don’t get a recession or the recession comes later, then its probable that AEO rallies up to $14 - $15 pretty quickly, as EPS moves from the $1.5 bogey close to $2.

From a technical perspective we have a lot of reasons to be bullish at this level. This is the all time chart for AEO:

It found support in this demand zone (9.82 - 11.6) nine times over the last 25 years. From this spot its rallied to at least 20 within the next 24 months seven times. Could this be the time that it breaks down even further? Possibly. But for that to happen either we’d need a horrible macro event, or Aerie growth would have to go negative quickly.

Management spent $191 million buying back shares last year. At current market cap prices that’s almost 9% of the float. I don’t think they’re going to buy back 9% of the shares outstanding this year, I do think they’ll buy back 160 - 175mm this year, which again should help support the stock. Especially at these levels.

There’s a lot to like here, a lot. This is a name I bought this week first after hours on Wednesday in small size, but then immediately put it on heavy on Thursday morning as the potential to get paid to wait and get a double in the next two years was enough to make me very excited. Which is why I think American Eagle is a stock you should at least look at, as it’s interesting.

Recession risk is going to be a major talking point topic through out 2025. At least for the first half. If it continues into the second half then its likely one is just around the corner. For now, when listening to conference calls consumer names, including AEO, have mentioned a slowing consumer. That could easily be explained away by where we came from in Q4 last year. With the fed cutting rates early and Trump bringing in tons of pro-growth optimism consumers felt like spending beyond their means wasn’t an issue. That obviously couldn’t continue forever, unless that optimism turned into results in the economy. It hasn’t. Yet. I’m going to do a long post on Trump in the next few days, so we’ll leave the political discussion for that, but the economy is clearly sluggish right now. The question is, is the pull back on a relative basis from Q4 into H1 2025 just a recalibration or the beginning of a nasty recession.

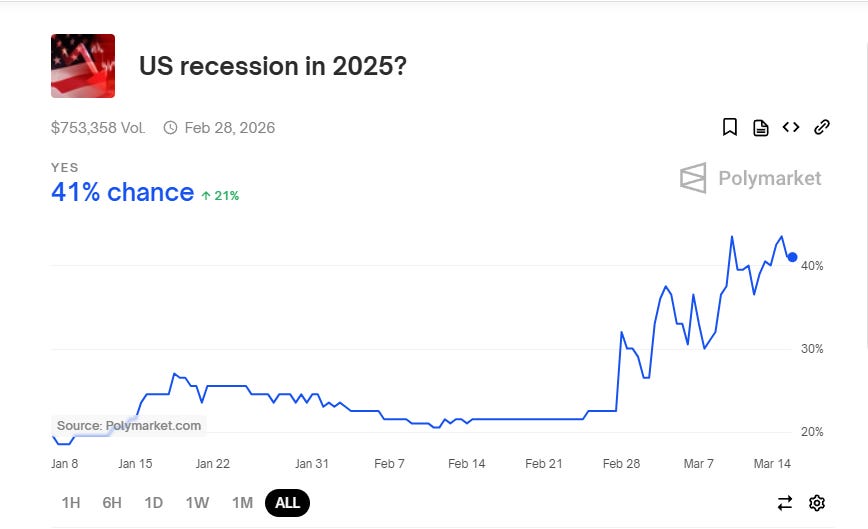

Polymarket betters think its the latter. Doubling the recession odds over the last 2 weeks.

This is very aggressive. 40% is very high. 20%, which is where it sat going into March is more likely the correct ‘fair’ number given where the economic data points sit right now. 40% is assuming the stock market knows something. If you’re a believer that the slowdown is just a recalibration and the consumer is fine, just not spending as aggressively, then 20% might even be high.

This all comes down to why you think the market is falling. Listen I’m not going to sit here and BS you and say everything is sunshine and rainbows with Delta and United both saying early indications of travel in late summer/fall are slower than expected. But again, given that travel has been on an absolute tear the last three years is a slow down from ‘peak travel’ a sign of a recession or just that the consumer is moving onto other things? But if the market is falling because of any reason that isn’t directly related to the consumer like dollar weakness, tariff/Trump instability, AI bubble valuations being popped, YoY growth being priced in at 18/19% and only coming it at 7% or five other reasons that come to the top of mind, then there’s a lot of heavily shorted stocks, mostly in the consumer focused space, that are about to explode higher given how heavily they’ve been shorted the last few weeks.

We will get some clarity on this topic Monday premarket with retail sales numbers coming out for February.

An example of the move higher is Peloton, which absolutely flew on Friday. 2nd highest non earnings volume in six months and up 15% on a pretty generic upgrade.

Now having cleared the 6.82 zone again, it’s likely heading back to 7.8, and above that it gets spicy again. I still very much like peloton, even in a minor recession, as it still is cheap if the turnaround is even 20% successful, but I’m not expecting any more 15%+ moves a day any time soon. At least not within any major news. Though if the broad market bounces it should continue higher.

That’s one of the two assumptions I’m making with the following stock suggestions, that the broad market is going to bounce (more on timeline below) and the second assumption is that while we need to keep a close eye on macro data near term recession risks need to come down a little bit.

Keep reading with a 7-day free trial

Subscribe to Sleepysol’s Newsletter to keep reading this post and get 7 days of free access to the full post archives.